Key Takeaways:

- The IDR waiver one-time account adjustment will occur automatically by July 1, 2024.

- Twelve months of consecutive forbearance (or more) or 36 months of total forbearance (or more) counted toward forgiveness.

- Any time spent in repayment (or qualifying periods of forbearance or deferment) counted toward forgiveness, even if you consolidated

- The IDR waiver applies to private-sector and public-sector workers.

- To qualify, some borrowers needed to consolidate their loans by April 30, 2024.

If you're a student loan borrower paying back your federal student loans using an income-driven repayment (IDR) plan, the Biden Administration's IDR waiver, also known as the IDR Account Adjustment, is a big deal. Any time you've spent in repayment and many periods of forbearance or deferment can now be counted toward the 10-year Public Service Loan Forgiveness and 20- or 25-year IDR forgiveness programs.

Millions of borrowers could see their entire balances wiped away completely. But unfortunately, many borrowers need to take action by the Administration's April 30, 2024, deadline.

Here's what we know about President Biden's IDR waiver program and how you can use it to shave years or even decades off of your student loan repayment journey.

If you need a customized plan to make the most of the IDR waiver, book a time with one of our top-rated student loan consultants.

One-time IDR account adjustment: What is the IDR waiver?

The IDR waiver is a one-time account adjustment by the Department of Education. It gives federal student loan borrowers credit toward forgiveness. All Direct Loan program borrowers, including graduate and Parent PLUS Loan holders, will receive at least three years of credit toward forgiveness.

Millions of borrowers who have been repaying their student loans for more than 20 years will automatically receive student loan forgiveness with this account adjustment (more on this below).

To do this, the U.S. Department of Education used its broad authority over student loans due to the pandemic national public health emergency. It results in extraordinarily generous changes to specific forgiveness programs that could get you out of student loan debt years sooner (or immediately).

The Department of Education previously enacted a Public Service Loan Forgiveness (PSLF) program waiver. Under this program, announced in October 2021 and expired at the end of October 2022, prior payments before consolidation were counted for loan forgiveness.

Payments made under any repayment plan counted, too, as long as you worked full-time for a nonprofit or government employer during the period in question.

The IDR account adjustment applies to a huge group of borrowers

With the IDR waiver, the Administration has broadened this assistance to a much larger group of borrowers and repayment statuses.

The PSLF waiver only helped public servants. Plus, it only awarded credit for the time a borrower was in an actual repayment plan.

All borrowers can now receive credit toward IDR forgiveness for any type of repayment plan, as well as qualifying forbearance periods and some types of deferment.

Like the PSLF waiver, borrowers with commercially-held debt with the Federal Family Education Loan program (FFEL) must consolidate to qualify.

The deadline for consolidation to take advantage of these benefits is April 30, 2024.

Borrowers with FFEL loans need to take action

We urge borrowers with commercially held FFEL loans to consolidate immediately.

If you have loans that weren't paused during the pandemic payment pause from March 2020 to September 2023 that show up when you log in to StudentAid.gov, then you have commercially held FFEL loans.

If you have this loan type, you should probably consolidate your debt before the deadline. Doing so could bring you very close to having your entire balance forgiven under these new rules.

Get Started With Our New IDR Calculator

Who will benefit from the IDR waiver?

The PSLF waiver only applied to borrowers in the public sector or who used to work in the public sector. But the IDR waiver now applies to ALL borrowers with federal student loans, meaning both private- and public-sector workers can benefit.

For borrowers pursuing PSLF, you can get credit toward your 10-year time requirement.

Borrowers not working toward PSLF can receive credit toward student loan forgiveness programs, like IDR forgiveness, over 20 or 25 years.

For example, if you have paid toward your undergraduate loans since 2006 and work in the private sector, you could consolidate before April 30, 2024, under the IDR waiver. In doing so, you can receive up to 17 years of IDR payment credit toward 20-year forgiveness under the Saving on a Valuable Education (SAVE) plan (formerly REPAYE).

You would only need three additional years of payments on an income-driven repayment plan. Then, your loan balance could be completely forgiven.

A physician who deferred her loans during residency for four years can get all four years counted toward the PSLF program now, thanks to the IDR waiver.

These examples show how the IDR waiver could help all types of borrowers regardless of employment status.

One minor IDR waiver caveat for PSLF borrowers

There's one minor limiting factor about the IDR waiver that I can find, and it only affects public sector borrowers. To receive total forgiveness for PSLF under the IDR waiver rules, you must work for a qualifying employer when the Department of Education makes the IDR Account Adjustment to your forgiveness credit.

The PSLF waiver didn't require you to work for a qualifying employer when they wiped your debt. So, that's slightly less generous.

Do deferment and forbearance periods qualify for loan forgiveness under the IDR waiver?

PSLF and IDR borrowers would receive credit toward forgiveness if they were in more than 12 months of consecutive forbearance. The same applies if you have 36 months of cumulative forbearance.

If you have less than 12 consecutive months of forbearance or 36 months or less of aggregate forbearance, then this credit doesn't qualify. In this case, you need to file a complaint with the FSA Ombudsman to review your situation.

Deferment before 2013 also counts for IDR and PSLF forgiveness, excluding in-school deferment. This is because the Department can't identify who was in economic hardship deferment and who wasn't. So, they're giving credit for all types of deferments.

For deferments after 2013, you must've been in a specific type of deferment. For example, active-duty deferment or economic hardship deferment are eligible. Most types of deferment qualify without a time requirement, as with the forbearance 12-month consecutive/36-month aggregate rule.

Notably, you can consolidate and still receive credit for qualifying periods of deferments and forbearances before the consolidation.

Great news: Time in any repayment plan now qualifies for forgiveness

The IDR waiver gives borrowers credit for any repayment plan toward IDR forgiveness, even payments made prior to consolidation.

For example, consider a borrower who has paid her loans under the Extended Repayment Plan since 2002. She would normally receive zero credit toward IDR forgiveness since the Extended Repayment Plan isn't based on income.

But under the IDR waiver, she could get credit for all those now-qualifying payments and either have her loans completely forgiven or be very close to forgiveness.

If she has loans with different payment histories, she could consolidate to get a very large amount of IDR credit on the new Direct consolidation loan based on the old repayment history of her oldest loan.

Related: How to Know If You Need a Consult with Student Loan Planner: 7 Situations to Consider

Most payment statuses pre-consolidation now qualify

Borrowers who made payments pre-consolidation can now get credit, too.

The Department of Education appears to be following the same game plan as it did for the PSLF waiver. Borrowers are getting credit for the loan with the most monthly payments applied to their overall consolidation loan.

Many borrowers can consolidate older loans and graduate degree loans to get much faster credit toward forgiveness overall.

The IDR waiver is even better than the PSLF waiver, as forbearance and deferment pre-consolidation can also count toward loan forgiveness.

Related: Student Loan Consolidation for Forgiveness: Do It Before or After the IDR Waiver?

How to consolidate federal loans to get the IDR waiver

To consolidate your federal student loans, go to the Direct Consolidation Loan Application on the StudentAid.gov website. Use StudentLoanPlanner.com/consolidate for an easy-to-remember shortcut.

Start by logging into your account and selecting the loans you want to consolidate. Be sure the boxes next to each of your loans have a checkmark. Your new Direct Consolidation Loan will reflect your selected loans, as shown below.

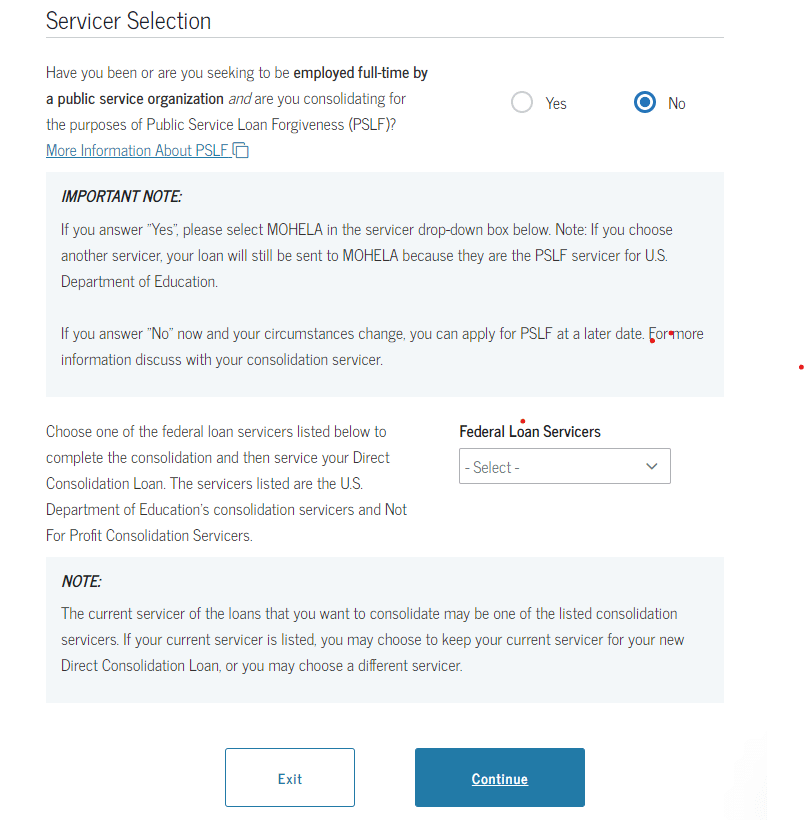

Then, select your preferred federal loan servicer. If you're pursuing PSLF, you must select MOHELA as your servicer. If not, we recommend sticking with your existing loan servicer.

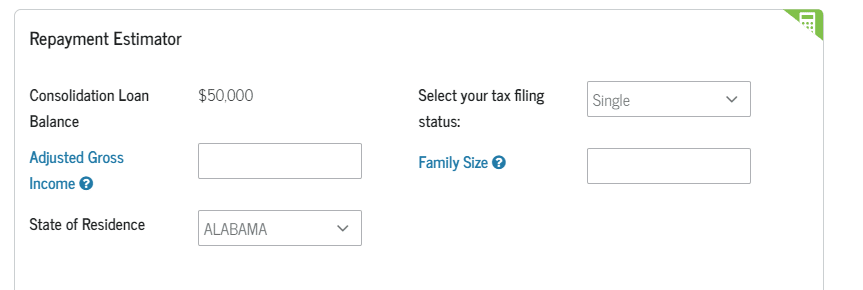

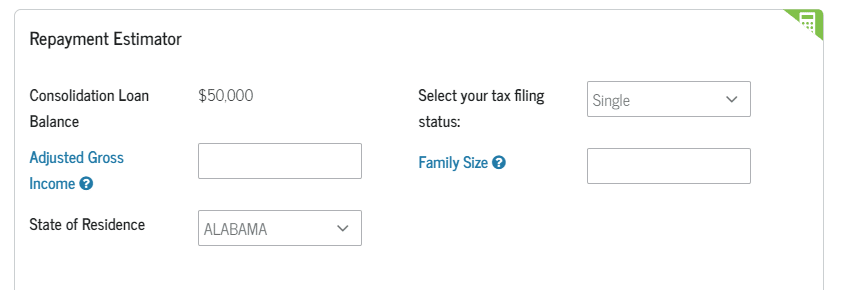

You'll then be able to enter your adjusted gross income, tax filing status, family size and state of residence. This information will generate estimated repayment information under each of the different IDR plans available.

Next, select your desired repayment plan. If you skip this step, your loan servicer will automatically apply the Standard repayment plan to your new loan.

From here, you'll finish the Direct Consolidation Loan application with additional questions about your employment and family details (e.g., number of dependents). You'll also need to provide income information. The easiest way to do this is to use the IRS Data Retrieval Tool.

Finally, you'll need to review the terms and conditions of the new consolidated loan and finish providing additional personal information. Then, review the application for accuracy and sign for the new loan.

Most borrowers with FFELs from before 2010 must take action

Borrowers with commercially held FFELP loans urgently need to consolidate before the deadline to qualify for the IDR waiver.

This is because program requirements prevent the Department of Education from granting credit automatically on this type of loan.

It's also possible that we'll see a lawsuit from investors to block relief for this type of loan.

As stated earlier, if you were still required to make payments during the student loan payment pause despite your student debt showing up on the Federal StudentAid.gov website, then you have this kind of student loan. You need to consolidate to receive credit under the IDR waiver.

Who will receive loan cancellation relief with the IDR waiver? Likely millions

According to the Department of Education, 3.4 million borrowers have been in repayment for at least 20 years. This is the minimum threshold to receive IDR forgiveness.

Most of these borrowers would not qualify for Pay As You Earn. Therefore, most would probably have to seek forgiveness under the SAVE plan rules. It allows for forgiveness after 20 years for undergraduate loans and 25 years for graduate loans.

“Several thousand borrowers with older loans will also receive forgiveness through IDR. More than 3.6 million borrowers will receive at least three years of additional credit toward IDR forgiveness,” said the Department of Education.

Saying “several thousand borrowers” and “at least three years of additional credit” is one of the biggest understatements in the history of the student loan program.

Million borrowers will receive complete cancellation thanks to the IDR waiver.

Tax implications of forgiveness under the IDR waiver

Until 2026, any cancellation is free from any federal taxation.

If you would receive forgiveness thanks to the IDR waiver within a few years of 2026, you might want to consult a tax advisor on ways to mitigate this potential tax impact. We expect taxation of cancelled and forgiven debt will depend on the outcome of the 2024 election.

A handful of states could impose state income tax, so consult a tax advisor if you live in any of the following states below if you receive forgiveness under the IDR waiver:

- Indiana

- Minnesota

- Mississippi

- North Carolina

Why the IDR waiver did not face a successful legal challenge

The IDR waiver has survived without any serious legal challenges being mounted.

We think borrowers with commercially held FFEL loans could have faced the most legal risk, as a lawsuit from an investor or group of investors could have blocked their access to this relief program.

Our best guess as to why we have not seen a successful conservative legal challenge to the IDR waiver is that conservative groups need a large enough payoff politically to justify going after the Biden administration in court. And blocking the IDR waiver is too technical and confusing to warrant a huge amount of effort to stop.

Get the most out of the IDR waiver for your situation

This IDR waiver could potentially accomplish a very large amount of debt cancellation. Some cancellations will be immediate. But much of it will also occur over the next several years as borrowers hit their 10-, 20-, and 25-year forgiveness payment counts, depending on the program they're eligible for.

Many borrowers will see their accounts automatically updated with a one-time revision late this year or early next. The Department of Education will instruct student loan servicers to make this update to your account. But your application could be processed much sooner if you obtain forgiveness under the IDR waiver before then.

For example, if forbearance and deferment, along with your payments, puts you above the 120 months needed for the PSLF program, you could fill out the PSLF ECF form and check whether you qualify immediately.

You could follow a similar process for 20- or 25-year IDR forgiveness, but with only a consolidation.

Decide whether or not you need to consolidate and take action

Many borrowers will want to consolidate to get the full benefits of the IDR waiver. But others with low IDR payments locked in until 2024 or even 2025, thanks to the student loan pause extensions, should not take any action.

What's clear is that the IDR waiver creates a massive number of opportunities for borrowers to save money. However, most are unaware of the possibilities for savings due to not understanding all the rules.

If you want assistance, we can help optimize your loan repayment strategy under the IDR waiver. Feel free to use tips from this article to get the most forgiven under this IDR account adjustment temporary program. We might not see another opportunity like this for student loan borrowers for years to come.

FAQ

The IDR waiver applies to all borrowers with federal student loans, including individuals in both public- and private-sector jobs. The PSLF waiver, which ended on October 31, 2022, was exclusively designed for current or former public sector employees. However, borrowers pursuing PSLF can take advantage of the IDR waiver to get credit toward the 10-year eligibility requirement for loan forgiveness.

Any federal student loan borrower can qualify for the IDR waiver. Borrowers who may benefit from this one-time adjustment include those previously or currently on an IDR plan, those participating in the PSLF program, or those interested in an IDR plan with Direct or FFEL Program loans held by the U.S. Department of Education (ED).

Borrowers do not need to apply for the IDR waiver, as federal loan servicers will update accounts automatically by July 1, 2024. However, some borrowers may benefit from consolidating their student loans to greater benefit from the IDR waiver.

Anyone who could get one or more years of additional credit towards forgiveness by consolidating their loans should do so at studentaid.gov. If you would get less than one year of additional credit, recertifying your IDR payment earlier than necessary would probably hurt you more than the additional forgiveness credit would help you.

President Biden's Plan B forgiveness would apply many of the benefits of the IDR waiver automatically. But this program will likely face legal hurdles.

It's very unlikely, as mass amounts of data would have to be reverted. Given how complex it would be to untangle all the consolidation histories and reverse these changes, a future administration would likely ignore the updates to payment counts made by this temporary Biden Administration program.

Not sure what to do with your student loans?

Take our 11 question quiz to get a personalized recommendation for 2024 on whether you should pursue PSLF, Biden’s New IDR plan, or refinancing (including the one lender we think could give you the best rate).

Comments are closed.