Since 2000, the average cost of college has more than doubled and outpaced inflation with annual growth of 7.1%. In recent years, in-state undergraduate yearly tuition has been $9,400; for out-of-state students, the cost is $27,300. That’s not including living expenses!

Fortunately, if you took out federal student loans for your undergraduate program, you can access forgiveness options through an income-driven repayment plan. This repayment strategy might save you tens of thousands of dollars on your student loan debt.

What is income-driven repayment (IDR) forgiveness?

As an undergraduate borrower, you might have access to IDR forgiveness. The only requirement for the program is that you make payments on one of the several IDR plans for 20 or 25 years, depending on the plan.

Those payments can be quite a bit lower than the fixed payments you’d make to pay your loans off. In fact, if you’re between work, the monthly payments might even be zero dollars! When you reach the end of the forgiveness period, any balance remaining on your loans is forgiven.

The current options for working toward IDR forgiveness on undergrad loans are:

| Payment plan | Term | Eligibility |

|---|---|---|

| Current Revised Pay as You Earn (REPAYE) | 20-year | Available to everyone |

| Pay as You Earn (PAYE) | 20-year | Only available if you took your first federal loan after October 1, 2007, and borrowed a loan after October 1, 2011 |

| ‘New’ Income-Based Repayment (IBR) | 20-year | Only available if you took your first federal loan after July 1, 2014 |

| ‘Old’ Income-Based Repayment (IBR) | 25-year | Available to everyone |

Why use IDR forgiveness for undergrad debt?

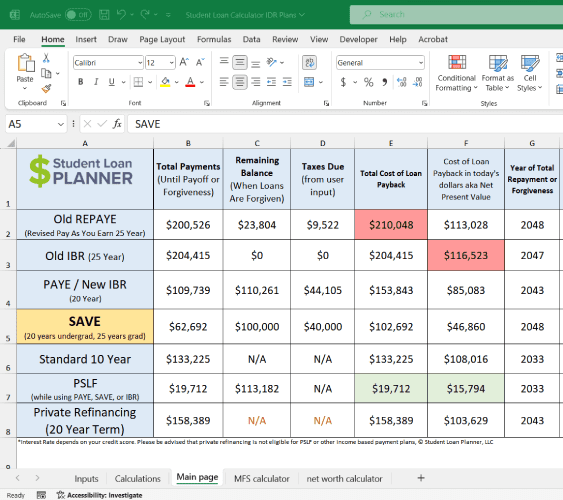

Let’s say you’re a borrower with a $50,000 federal loan balance from your undergrad. At 6%, your fixed payments in the federal system to pay the loans off over 25 years would be $322 per month.

Now, let’s say you’re single, earning $40,000 annually, and saving $3,000 per year in a workplace 401(k) plan. Your monthly payments under the current REPAYE plan, for example, would only be $126 — that’s 60% less! Not only would you substantially reduce your payments, but you’d also get rid of your loans in 20 years instead of 25 years with the fixed payment.

What’s also very powerful is that the Department of Education bases your payments on your adjusted gross income (AGI), not your total income. Since any retirement contributions to a traditional workplace retirement plan lower your AGI, you can save more for retirement to partially or fully offset increases in your income over time.

This allows you to prioritize retirement savings while also paying less on your loans under an IDR plan.

Get Started With Our New IDR Calculator

How you qualify for IDR forgiveness

To qualify for the lowest-cost options while working toward IDR forgiveness, you need to have federal Direct Loans. This allows you to use PAYE, REPAYE, and the new version of IBR, all of which offer payments based on 10% of discretionary income with a 20-year term.

If you have Federal Family Education Loan (FFEL) program loans (possible only if you took out loans before 2010), you can still work toward IDR forgiveness. However, you’re limited to only using the old version of IBR.

This plan has higher payments based on 15% of discretionary income and a 25-year forgiveness term. If you have Perkins Loans, they aren’t eligible for IDR forgiveness. If you have either of these loan types, consider consolidating them to a Direct Loan under the IDR waiver. This opens up lower-cost options for you.

What about your spouse’s income?

You probably noticed that the current REPAYE plan has low payments and offers 20-year forgiveness to borrowers with Direct Loans. Why would anyone bother with PAYE or New IBR? The answer comes down to how your spouse’s income is considered.

With the current REPAYE plan, your spouse’s income is always factored into the monthly payment. In keeping with the scenario mentioned above, let’s say you got married and your spouse has the same annual income of $40,000. They also contribute $3,000 to their 401(k) plan. On the current REPAYE, your monthly payment would jump from $126 as a single borrower to $370 per month as a married borrower. Now it’s more expensive than your original fixed payments.

If you’re eligible for the PAYE or New IBR plans, you and your spouse could file taxes as “married, filing separately,” so your payment is calculated based only on your income. You’d even get to keep the 20-year forgiveness term.

If you borrowed your first loan before October 2007, you could still exclude your spouse’s income by using the old IBR plan, but there are two trade-offs. Your payments would be slightly higher compared to being single on REPAYE, and you would have a 25-year term instead of a 20-year period.

How New REPAYE changes things for Undergrad Degree Holders

The New REPAYE plan is a “facelift” for the current REPAYE with many changes — all for the better. It’s expected to launch in late-Summer or Fall 2023. The new plan offers undergrad borrowers lower monthly payments due to:

- A lower definition of discretionary income from a 225% deduction of the poverty line for your family size (vs. 150% on the other plans).

- A lower payment calculation of just 5% of discretionary income for undergrad loans (vs. 10% or even 15% on the other plans).

Borrowers would also have the flexibility to exclude their spouse’s income by filing taxes separately under New REPAYE, whereas the current REPAYE doesn’t provide that option. Even with all these benefits, the forgiveness term remains at 20 years for undergrad borrowers.

Sticking with our example, despite a combined income of $80,000 per year from you and your spouse, if you filed your taxes separately and enrolled on the New REPAYE plan, your IDR monthly payment would be $35. This is a massive reduction compared to a 25-year fixed payment of $322 per month.

Lastly, the New REPAYE plan offers a 100% subsidy of any interest that would normally be charged above your monthly payment. So in our example, $50,000 in loans with a 6% interest rate accrued $250 per month in interest. On the PAYE and IBR plans, if you have a required monthly payment that doesn’t cover all of the $250 each month, then the loan balance would accrue interest and grow. On New REPAYE, if your monthly payment is $35, the unpaid interest of $215 per month is completely waived.

This ensures that your loan balance will never grow as long as you’re making your income-driven payments. It’s important to keep the balance from growing because the forgiven amount might be taxed.

Planning for the “tax bomb”

When you reach the end of IDR forgiveness, the balance of your loans that gets forgiven is considered taxable income to you. You pay taxes on this balance at your marginal rate, likely 20% to 30%. This means that a balance of $50,000 forgiven would result in roughly $12,000 in taxes, assuming you’re in the 24% tax bracket.

Prepare for these taxes in the same way you’d prepare for a big upcoming purchase: by saving and investing. We’ve found it easiest to save a set amount each month into an account where it can be invested to grow for this future tax bill. It’s best to consider this just another part of your monthly student loan payment that’s sent to your own investment account instead of a servicer.

It’s important to note that for borrowers getting IDR forgiveness between now and the end of 2025, the forgiveness isn’t taxable due to the American Rescue Plan enacted in 2021.

Is IDR forgiveness the best option for getting rid of your undergraduate loans?

Whether it’s best for you to work toward IDR forgiveness, or pay them off instead, is determined by multiple variables. These include how much forgiveness credit you already have, the types of loans you have, and your current and expected future income.

If you’ve recently graduated and expect to earn an annual income that’s similar to your loan balance, working toward IDR forgiveness will likely save you thousands. What’s more, if your income increases, you can simply save more in your workplace retirement plan (up to $22,500 per year in 2023) to lower your AGI, and thus, your IDR payments.

If instead, your income upon graduating is already 1.5 times your loan balance, you would likely benefit from paying the loans off as quickly as possible. This would save money compared to your income-driven payments and the taxes due upon forgiveness.

Let us help

At Student Loan Planner, we help borrowers answer the question of how to get rid of their loans as economically as possible. Every borrower’s situation is different, and we almost always find that choosing the right approach saves thousands.

If you’re unsure whether IDR forgiveness will save you money, book a consultation, and we’ll work with you to create a fully customized plan.

Not sure what to do with your student loans?

Take our 11 question quiz to get a personalized recommendation for 2024 on whether you should pursue PSLF, Biden’s New IDR plan, or refinancing (including the one lender we think could give you the best rate).