If President Trump wins the 2024 election, will he seek to repeal the Saving on a Valuable Education (SAVE) repayment plan? Right now, it seems more likely than not that he would.

We’ll discuss how a SAVE plan repeal would happen if Trump wins and what options borrowers might have for their student loan debt as a result.

Why President Trump would oppose SAVE

At first glance, President Trump’s first term saw almost no movement on student loan policy besides pausing federal student loan payments and interest at the beginning of the pandemic. Given that he expressed very little interest in student loan policy, why would it be a foregone conclusion that Trump would oppose the SAVE plan in a second term?

The best evidence is the strong Republican opposition to SAVE at the state level.

Multiple Attorneys General from Republican-led states have filed lawsuits against President Joe Biden’s SAVE plan. In total, 18 states have joined some version of these lawsuits.

Clearly, stopping the SAVE plan is an animating policy issue among Republican officials.

While President Trump was unmotivated to launch a new income-driven repayment (IDR) plan during his term, stopping an existing IDR plan would be easier to accomplish.

Get Started With Our New IDR Calculator

How Trump would repeal the SAVE plan

Ending the SAVE plan would likely require a negotiated rulemaking session. The President Biden Administration took a similar approach in implementing the SAVE plan in the first place.

Negotiating rulemaking is a fancy word for a formal committee representing key stakeholders affected by a policy change. If the committee approves the proposed regulatory changes Department of Education suggests, the regulations go into effect. If the committee can’t come to a consensus, the Department of Education can do whatever it wants.

The most obvious path to repealing the SAVE plan would be to replace it with the IDR plan specified in the College Cost Reduction Act.

What would replace SAVE?

That IDR plan, which we might call the GOP IDR plan, is quite similar to the Revised Pay As You Earn (REPAYE) plan, except there’s a component that matches a borrower’s monthly payments made on interest to the principal.

This plan is significantly less generous for low-income earners, but it’s more generous than the REPAYE plan.

It’s possible that a Trump-led Department of Education would simply reintroduce the REPAYE plan instead, but replacing it with something designed by Republicans seems more likely.

Could SAVE be protected in a legislative compromise?

It’s probably true that Republicans care more about other issues like tax policy than education policy. Hence, if Democrats control Congress — either the House or the Senate — with the Trump tax cuts expiring in 2026, Republicans could be willing to trade something like not repealing SAVE for concessions on extending part of the Trump tax cuts.

Additionally, tax-free forgiveness, which was implemented under the 2021 American Rescue Plan, expires in January 2026. Significant horse-trading over education policy could make the future of SAVE somewhat hard to predict.

Why repealing SAVE would be very easy

Ultimately, the White House can convene a negotiated rulemaking session for any reason, and that committee has extremely wide latitude over regulations on IDR, particularly under the Income Contingent Repayment (ICR) statute.

President Obama used that ICR statute to create the Pay As You Earn (PAYE) and REPAYE programs.

So, when asking the question, “Would President Trump repeal SAVE?” you might simply consider how easy or difficult that policy action would be.

Since it merely requires a regulatory committee convening, it’s very likely that SAVE would be repealed.

How fast could SAVE be repealed?

Hypothetically, if Donald Trump wins in 2024, the negotiated rulemaking committee can’t meet until he is sworn in in early 2025.

For new rules to take effect in July 2026, they’d need to be published by November 2025. However, rulemaking committees require public notice and comment, so it’s possible that the committee could convene at least until 2026. That would mean SAVE couldn’t be repealed until July 2027.

Any change would not happen overnight. And if a Democrat wins in 2028, then a president could use negotiated rulemaking to make an even more generous plan than SAVE.

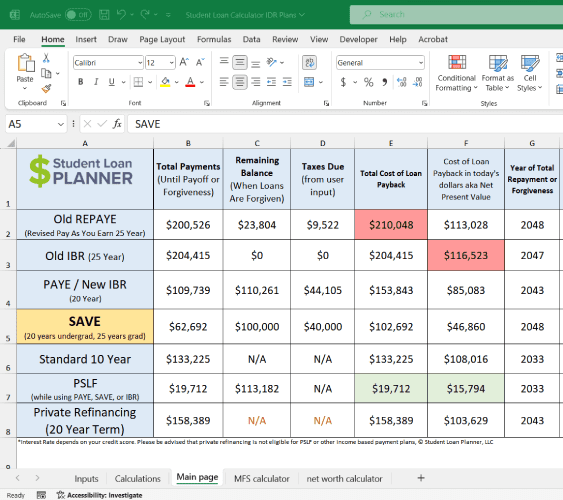

What can borrowers do to prepare for SAVE getting repealed

Generally speaking, a student loan borrower who needs to go for forgiveness on SAVE would still need to go for a student loan forgiveness plan on whatever version of IDR a future President creates.

There are exceptions, but that rule applies to the majority of borrowers.

It’s important to know what’s written into law and cannot be reversed without 60 votes in the Senate.

Specifically, the Income-Based Repayment (IBR) statute defines “Old IBR” as 15% of a borrower’s income for 25 years of payments and New IBR as 10% of income for 20 years. “New IBR” is only available to borrowers who took out a loan for the first time after July 2014.

So, it might be helpful to understand your worst-case scenario as a borrower. If that scenario still involves going for debt forgiveness, then you’re in good shape.

If you want to chat about a customized plan in case of SAVE plan repeal, you can book a time with our team of experts.

Refinance student loans, get a bonus in 2024

| Lender Name | Lender | Offer | Learn more |

|---|---|---|---|

|

$500 Bonus

*Includes optional 0.25% Auto Pay discount. For 100k or more.

|

Fixed 5.24 - 9.99% APR*

Variable 6.24 - 9.99% APR*

|

|

|

$1,000 Bonus

For 100k or more. $300 for 50k to $99,999

|

Fixed 5.19 - 10.24% APPR

Variable 5.28 - 10.24% APR

|

|

|

$1,000 Bonus

For 100k or more. $200 for 50k to $99,999

|

Fixed 5.09 - 9.74% APR

Variable 5.89 - 9.74% APR

|

|

|

$1,050 Bonus

For 100k+, $300 for 50k to 99k.

|

Fixed 5.44 - 9.75% APR

Variable 5.49 - 9.95% APR

|

|

|

$1,275 Bonus

For 150k+, $300 to $575 for 50k to 149k.

|

Fixed 5.48 - 8.69% APR

Variable 5.28 - 8.99% APR

|

|

|

$1,250 Bonus

For 100k+, $350 for 50k to 100k. $100 for 5k to 50k

|

Fixed 5.48 - 12.43% APR

Variable 5.28 - 12.43% AR

|

Not sure what to do with your student loans?

Take our 11 question quiz to get a personalized recommendation for 2024 on whether you should pursue PSLF, Biden’s New IDR plan, or refinancing (including the one lender we think could give you the best rate).