Student loan borrowers have been experiencing significant turbulence, with the landscape constantly shifting beneath their feet. New student loan forgiveness and repayment programs, many with complicated eligibility criteria and disparate timelines, offer borrowers opportunities for relief and confusion. The path for borrowers appears to be ever-changing, leaving many feeling lost and unsure of their next steps.

Here are the latest shakeups impacting student loan programs and what borrowers need to know about them.

Loan forgiveness under PSLF program is officially paused

As of May 1, 2024, the Public Service Loan Forgiveness (PSLF) program is officially paused. This temporary interruption is part of a broader Education Department plan to transition several student loan forgiveness and discharge operations handled by individual servicers to the StudentAid.gov platform. That way, borrowers can access key programs regardless of who their servicer is.

Uncle Sam takes over PSLF processing

In the case of PSLF, the department is moving servicing from MOHELA — which took over PSLF operations from FedLoan Servicing during the COVID-19 pandemic — to StudentAid.gov. During the transition period, which is expected to last until July, borrowers will have no access to their PSLF data. The department will not process any PSLF Employment Certification forms and will not grant any loan forgiveness.

“As a federal contractor for the U.S. Department of Education, Office of Federal Student Aid, MOHELA will be supporting the government on its planned transition of servicing of the PSLF Program to StudentAid.gov,” said a MOHELA spokesperson in April. “The decision to transition PSLF servicing to FSA was a years-long strategy first announced by the Department back in 2022, prior to MOHELA becoming the interim PSLF servicer, with FSA's long-term goal of a transition always set to take place around this time.”

Related: PSLF on Pause: How to Survive Loan Forgiveness Delays and Errors

Once the PSLF suspension ends in July, borrowers should be able to access their PSLF data again through a new dashboard on StudentAid.gov. The department will then resume PSLF processing.

Borrowers can submit PSLF employment forms during the pause, but advocates recommend doing so online using the PSLF Help Tool. Given anticipated backlogs once the suspension ends this summer, buckle up for a long processing period.

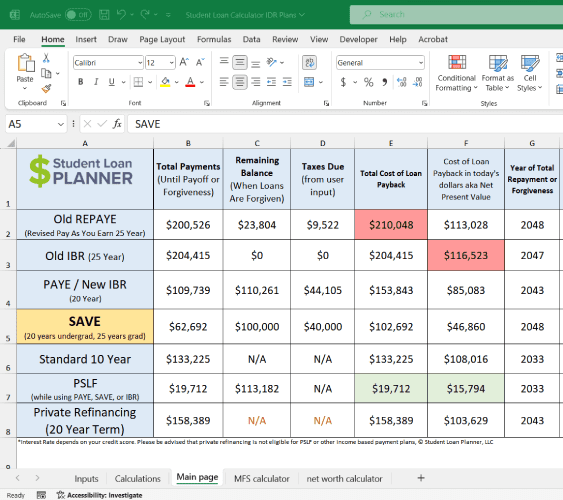

Get Started With Our New IDR Calculator

MOHELA's musical chairs

While all borrowers on track for PSLF will no longer access their PSLF data through MOHELA, many borrowers will continue to have their student loans serviced by MOHELA. But not all.

Last month, the Education Department announced that MOHELA would be transferring hundreds of thousands of borrowers to other department servicers such as Nelnet, EdFinancial and Aidvantage.

“As part of this ongoing work to improve borrowers’ experiences, this week FSA will begin transferring a portion of MOHELA’s borrower accounts to other federal student loan servicers,” said the department in an announcement in April. “A different servicer will begin managing these loans and assisting these borrowers so that they can benefit timely from improvements that are being implemented this summer.” MOHELA had requested the transfer, the department noted.

At least a million borrowers are expected to be impacted by the transfers. MOHELA and the Education Department will notify borrowers who are subject to the shakeup. Once the transfer is complete, borrowers may need to establish a new online account and set up payments with their new loan servicer.

Related: MOHELA Student Loans Review: 5 Biggest Complaints About This Servicer

Key federal student loan official steps down

In another major shakeup, Richard Cordray, Chief Operating Officer at the Office of Federal Student Aid, announced he would be stepping down last month. FSA oversees the entire federal student loan system, including federal student loan forgiveness and repayment programs.

Cordray's curtain call

“We are grateful for Rich Cordray’s three years of service, in which he accomplished more transformational changes to the student aid system than any of his predecessors,” said Education Secretary Miguel Cardona. “He undertook the work of fixing the broken student loan system programs like Public Service Loan Forgiveness and Income Driven Repayment, identifying 4 million borrowers who were eligible for loan forgiveness.”

“Richard Cordray’s leadership was transformational. Since starting his tenure in 2021, he improved the application process for programs like Public Service Loan Forgiveness and Income Driven Repayment, helping millions of eligible borrowers receive relief,” said Michael Calhoun, president of the Center for Responsible Lending, in a statement. “He also oversaw the development and implementation of the most affordable student loan repayment plan to date, the SAVE Plan, and fought arduously to prevent predatory lending practices in higher education.”

Cordray, who previously oversaw the federal Consumer Financial Protection Bureau, will continue working at FSA through the end of June.

The IDR account adjustment deadline has passed

Meanwhile, April 30, 2024, was the final deadline for certain borrowers to consolidate their loans via the federal Direct consolidation program to benefit from the IDR account adjustment. This temporary initiative can allow borrowers to get credited with time toward 20-year or 25-year loan forgiveness under income-driven repayment plans.

While many borrowers will automatically receive the benefits of the account adjustment, borrowers with commercially owned FFEL loans and other federal student loans not held by the Education Department must have applied to consolidate through the Direct lending program by April 30 to get the program's full benefits. Advocates had hoped the department would extend the deadline at the last minute (which the department did in the past), but that did not happen.

Under the IDR account adjustment, borrowers can preserve (and even increase) their loan forgiveness credit if they applied to consolidate by the deadline. But with this crucial deadline now expired, borrowers who apply to consolidate now could risk losing their existing IDR credit (if they have any).

What now for borrowers?

Starting on July 1, 2024, borrowers who consolidate and enroll in the new Saving on a Valuable Education (SAVE) plan will receive the weighted average of existing IDR credit based on the repayment histories of the underlying loans. However, borrowers who haven’t yet consolidated their loans should be cautious about doing so before July 1, 2024.

Not sure what to do with your student loans?

Take our 11 question quiz to get a personalized recommendation for 2024 on whether you should pursue PSLF, Biden’s New IDR plan, or refinancing (including the one lender we think could give you the best rate).