As an educator, you have several options to get teacher loan forgiveness. Having your student loan debt wiped out seems like a good thing, but you need to know what you’re getting into when you pursue loan forgiveness.

Each federal loan forgiveness program has different qualifications and guidelines. The right program for you depends largely on your total amount of debt, current and future employment and life goals. Certain tax implications could even affect whether a forgiveness option is right for you.

Is teacher loan forgiveness even the best option to handle your student loan debt? Read on to learn about student loan forgiveness for teachers and other options to pay off your student loans.

Get Started With Our New IDR Calculator

Teacher Loan Forgiveness has narrow benefits

The federal Teacher Loan Forgiveness Program is popular among teachers looking for relief from their student loan debt. However, it's designed to encourage borrowers in the teaching profession to work in areas with a shortage of qualified teachers. So, the program has strict requirements.

You can qualify for up to $17,500 in loan forgiveness after working five consecutive academic years as a full-time teacher in a low-income qualifying school or educational service agency if you meet additional eligibility requirements.

For teachers outside of those requirements, you might still qualify for loan forgiveness help but only up to $5,000.

Are you eligible for the Teacher Loan Forgiveness program?

Here are the main requirements for Teacher Loan Forgiveness, according to Student Federal Aid, an Office of the U.S. Department of Education:

- You must have taught full time for five complete and consecutive years. One of those years must have been after the 1997-98 academic year.

- You must be a highly qualified teacher at a qualifying school. Use this Teacher Cancellation Low Income (TCLI) directory to search for your school or agency.

- Your loan(s) must be from before the end of your five-year period of qualifying teaching service.

Who is considered a highly qualified teacher? A highly qualified teacher is one who:

- Has received a bachelor’s degree

- Maintains full state certification in the state where they teach

- Hasn't had any licensing or certification requirements waived for any reason

If you are a highly qualified special education teacher at the elementary or secondary education level or a secondary mathematics or science teacher, you may qualify for up to $17,500 in forgiveness.

Other teachers of any grade level can receive up to $5,000 in loan forgiveness.

Teachers can apply for loan forgiveness after completing the five-year period teaching requirement. Note that PLUS loans and Perkins loans are not eligible for the Teacher Loan Forgiveness program.

For more detailed information on this particular type of student loan forgiveness for public and private school teachers, visit the Federal Student Aid website.

If you’ve confirmed your eligibility, you need to fill out the Teacher Loan Forgiveness Application. Be aware that one of your school administrators (e.g. superintendent or human resources staff) will need to complete a section of the form. If you have qualified full-time employment at multiple qualifying schools, you'll need the “chief administrative officer” of each site to complete the section.

Public Service Loan Forgiveness for teachers

Teachers looking for student loan forgiveness options also can look into Public Service Loan Forgiveness (PSLF). According to the Department of Education, PSLF “has the broadest employment qualification requirements of the federal programs listed — it doesn’t require that you teach at a low-income a public school or even be a teacher. Most full-time public and private elementary and secondary school teachers will meet the employment requirements.”

PSLF is a federal student loan forgiveness open to anyone with qualifying Federal Direct Subsidized or Unsubsidized Loans and who meets all the program requirements. Those requirements are:

- Have student loans through any federal income-driven repayment programs.

- Make 120 qualifying payments on your student loan. A qualifying payment is one that is paid on time and in full. The 120 payments do not need to be consecutive.

- Work for a government or qualifying employer while making qualifying payments, as well as during the application process.

Which repayment plans qualify for PSLF?

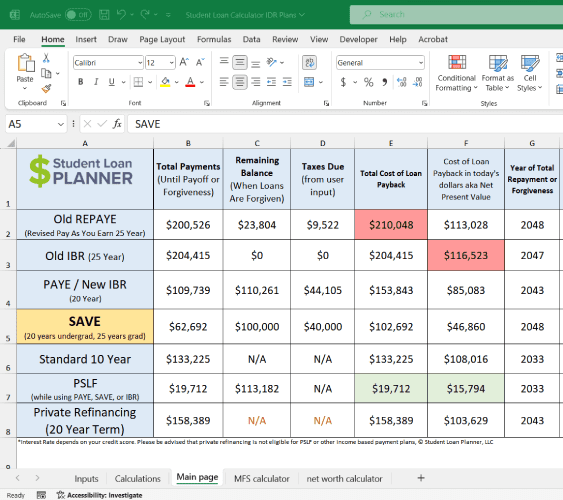

All four income-driven repayment (IDR) plans qualify for PSLF, including the Saving on a Valuable Education (SAVE), Pay As You Earn (PAYE), Income-Based Repayment (IBR) and Income-Contingent Repayment (ICR). Note the new SAVE plan replaced the old REPAYE plan, but it now includes more generous borrower benefits such as a larger poverty line deduction and lower payments for borrowers with undergraduate loans.

Technically, the standard 10-year payment plan qualifies for PSLF as well. However, your student loan payments aren’t lowered within the Standard Repayment Plan. So, your student loan debt would be paid off by the time you reached 120 payments.

Other repayment plans that do not qualify for PSLF include the:

- Graduated Repayment Plan

- Extended Repayment Plan

- Alternative Repayment Plan

PSLF requires you to have Direct loans. If your student loans are non-Direct federal student loans, you’d need to first consolidate them into a Direct Consolidation Loan. If you have both types of loans, it's best to only consolidate your non-Direct loans. Any payments made on your Direct loans prior to consolidating would no longer count toward your 120-loan-payment count.

Although some student loan forgiveness programs are taxable, PSLF is not. Forgiven loans aren’t considered income by the Internal Revenue Service.

To apply for PSLF, you need to fill out and submit the PSLF Application for Forgiveness. Another important step in qualifying for PSLF is submitting the Employment Certification Form annually, as well as any time you change employers.

Teacher Loan Forgiveness vs. PSLF

Any teacher with student loans would love an easy way to wipe out that debt and create more financial freedom. Debt elimination would not only remove a giant stress in your life but also free up money for other life goals like buying a home, starting a family and saving for retirement.

Federal teacher loan forgiveness has strict requirements to be eligible for the full $17,500 in loan forgiveness. The alternative $5,000 option is helpful. But if you have over $25,000 in student loan debt, you'll still have a hefty remaining balance to pay off.

Another potential issue is not picking the right program and sabotaging your chances for more funds. Technically, you can receive loan forgiveness through the Teacher Loan Forgiveness Program as well as PSLF. But there is a catch.

According to the Federal Student Aid website, “you can potentially receive forgiveness under both the Teacher Loan Forgiveness Program and the Public Service Loan Forgiveness Program, but not for the same period of teaching service.”

In other words, if you work for five qualifying years to receive Teacher Loan Forgiveness, you can’t count any of the payments made during that time period toward your required 120 qualifying payments for PSLF. This rule adds five more years of payments to your financial strategy if you wanted to pursue both programs.

How to choose between loan forgiveness options

Considering the rule that payments made for the Teacher Loan Forgiveness Program can’t also count as PSLF payments, it would make more sense to just start out pursuing PSLF instead of Teacher Loan Forgiveness. PSLF is less strict in regard to teaching qualifications. But it also would wipe out your entire student loan debt, not just a portion of it.

A drawback to PSLF, though, is that you need to make 10 years of qualifying payments in order to be eligible. What if your career goals change or you decide to stop teaching? A lot can change in the life of a teacher in 10 years.

Related: Teacher Loan Forgiveness vs. Public Service Loan Forgiveness for Teachers: Which Is Better?

Why PSLF is usually better than Teacher Loan Forgiveness

Imagine you're a teacher with $50,000 in student debt. You're a highly qualified math teacher at the high school level. You could get $17,500 in total forgiveness.

You earn $40,000 per year, have two kids and a spouse who earns about the same amount of money as you do. Your spouse has no student debt.

You could go for the Teacher Loan Forgiveness Program and earn $17,500 forgiven in the first five years. Of course, you'd still have a $32,500 balance leftover. Then you'll need to make payments for an additional 10 years to have your loans forgiven through PSLF. You can't double-count service for both programs.

Pursue PSLF from the beginning

Instead, you could forgo Teacher Loan Forgiveness and just utilize PSLF from the start.

If you filed married filing separately for taxes and had inflation level raises on your $40,000 salary, your first Pay As You Earn (PAYE) payment as a teacher would be $74 a month.

Over 10 years, you'd pay a total of $10,123 under PSLF as a teacher.

By comparison, if you did Teacher Loan Forgiveness, you would have $17,500 wiped away, but you'd still owe your balance plus whatever interest had accrued.

You're better off paying $10,000 over 10 years toward PSLF than being left with $30,000 to $40,000 after Teacher Loan Forgiveness.

Hence, Teacher Loan Forgiveness is pretty useless if:

- You plan on having a career in teaching.

- You owe more than $30,000.

- The debt you have is mostly federal student loans.

It's ironic the program named for teachers is useless for most teachers compared to the more generically named PSLF program.

PSLF and Teacher Loan Forgiveness are the most common programs for loan forgiveness. But teachers have other options, too. Picking the right option will depend on your specific situation, with each program having benefits for certain teachers.

Other loan forgiveness options for teachers

Teachers looking for relief from student loans have other options available. Factors like what type of student loans you have and where you reside play a role in determining which programs are available to you.

Federal Perkins Loan cancellation

If you have Perkins loans, you can potentially have your loans canceled up to 100% through the Federal Perkins Loan Cancellation program. In order to qualify, you must be:

- A teacher serving students of low-income families; or

- A special education teacher (including teachers of infants, toddlers, children or youth with disabilities); or

- A math, science, foreign language or bilingual education teacher or be a teacher in another field in one of your state's teacher shortage areas.

To find out if your school of employment is classified as a low-income school, check the federal TCLI directory.

Up to 100% of the loan may be canceled for full-time teaching service based on the number of years of service you have. Here are the tiers of service-based cancellation through the federal Perkins loan program:

- 15% canceled per year for the first and second years of service

- 20% canceled for the third and fourth years

- 30% canceled for the fifth year

Any canceled amount includes interest accrued during that year of service.

For more information and to apply for Perkins Loan Cancellation, teachers need to contact the school that made the loan or to the school’s Perkins Loan servicer.

Income-driven repayment plans

If you are a teacher who doesn’t qualify for one of the other federal loan forgiveness options listed above, there is another way to get your loans forgiven. You would need to move your student loan payments to one of the four eligible income-driven repayment options.

Under an IDR plan, after making payments for 20 to 25 years, any remaining student loan debt is forgiven. The four IDR plans are:

- Saving on a Valuable Education (SAVE) – formerly REPAYE

- Pay As You Earn (PAYE)

- Income-Based Repayment (IBR)

- Income-Contingent Repayment (ICR)

The drawback to pursuing this type of loan forgiveness is that there are potential tax implications when your loans are forgiven. Because forgiven loan debt through IDR is considered taxable income, you might face a hefty tax liability — do your research and weigh the pros and cons before making any decision to pursue teacher loan forgiveness this way.

State-based loan repayment programs

In addition to federal loan forgiveness programs, certain individual states have teacher cancellation benefits to help educators pay off student loan debt. Programs vary from state to state. Here are two available state-based programs:

Illinois Teachers Loan Repayment Program

The Illinois Teachers Loan Repayment Program allows for teachers working in the state to receive up to $5,000 if they already received funds through the federal loan forgiveness program but still have a balance remaining on their loans. Teachers have to fulfill their five-year teaching obligation in an Illinois elementary or secondary school designated as a low-income school.

My family’s experience with loan forgiveness for teachers

My wife, Barb, is a public school teacher in Ohio who has been teaching for over 17 years. When she pursued her bachelor’s degree, she accumulated some undergraduate student loan debt. It wasn’t very much, and she paid it off quickly.

More recently she decided to pursue a master’s degree in special education. She needed to take classes in order to renew her teaching license in Ohio. She also wanted to expand her teaching options and move up a pay grade. After graduating from Baldwin Wallace University in Berea, Ohio, with her master’s in special education, she ended up with $19,270 in student loan debt.

Related: Are Advanced Degrees Worth It for Teachers?

At the time, neither of us was familiar with any options for student loan debt other than just paying it off through the Standard Repayment Plan. One of her colleagues told her about the federal Teacher Loan Forgiveness Program.

We tried pursuing the maximum forgiveness of $17,500, but she didn’t qualify because she wasn’t in a teaching role that lined up with her master’s degree. She did, however, qualify for $5,000 loan forgiveness through the program and was approved for forgiveness earlier this year. She’s now free of student loan debt.

While it’s great we're out from under those monthly student loan payments, we wish we were better informed about what was available. Most likely she would have qualified for PSLF, which would have lowered the amount we had been paying monthly and then wiped out all of her remaining student loan debt, not a portion of it.

Our lesson: It was our fault that we didn’t seek out help to not only understand our options but also determine the best repayment option for our situation.

What is the best option for paying off your student loan debt?

With all of the options available for teacher loan forgiveness, you have a lot of information to digest and decode in order to find the right fit for your situation. Just as teachers are experts at educating students, the consultants at Student Loan Planner® are experts at educating our clients and working with them to find the right payment options.

If you want help saving money and getting out from under your teacher student loan debt, book your student loan consultation today.

Has teacher student loan forgiveness been worth it for you?

Not sure what to do with your student loans?

Take our 11 question quiz to get a personalized recommendation for 2024 on whether you should pursue PSLF, Biden’s New IDR plan, or refinancing (including the one lender we think could give you the best rate).

Comments are closed.