If you’re a chiropractor, or want to become one, you should know about the extreme unfairness toward the profession that exists today. Chiropractors are treated horribly under student loan rules.

Students who graduate with huge chiropractic student loan balances aren't eligible for the best forgiveness options. They also don’t earn high enough incomes to pay back their debts.

To top it off, their higher-earning MD peers have access to a massive loophole in the student loan rules that chiropractors do not. This will result in chiropractors paying hundreds of thousands of dollars more on their student loans than health care practitioners making three times their salaries.

This piece should serve as a call to action for the chiropractic profession. If you've got chiropractic debt, check out our free Student Loan Calculator and keep reading to learn about your repayment options.

Get Started With Our New IDR Calculator

Chiropractors' student loan balances are among the highest of any profession

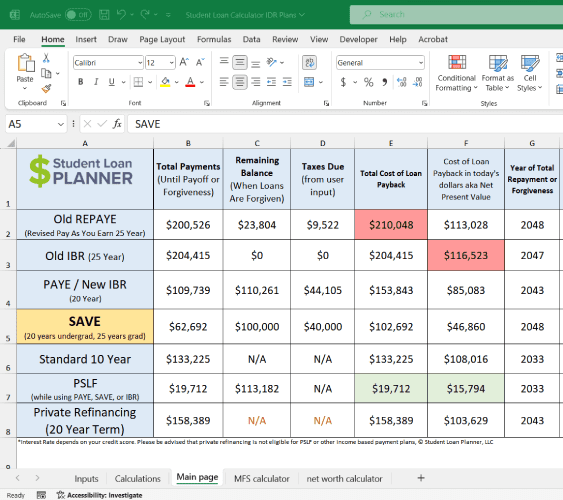

I’ve worked with many chiropractor borrowers since starting Student Loan Planner®. We regularly see an average debt of $250,000 for chiropractor student loan debt, with some being much higher. This is wrong for so many reasons.

First, the average med school graduate we help has a lower balance. Regardless of what schools tell you, it has to be more expensive to educate a med student than a chiropractic student. Why do chiropractic educations cost so much then?

One reason is there’s not many accredited chiropractic schools to choose from. The ones that are around are typically private or for-profit institutions, like Palmer College of Chiropractic in Davenport, Iowa.

Furthermore, the federal government doesn't impose any caps for practical purposes on how much student debt you can borrow. That means the schools that do exist have an unlimited amount of federal and private student loans they can sign students up for. If you've already gotten through your first year of chiropractic college, you're probably going to stick around and accept whatever tuition increases they throw at you.

In the absence of any market-imposed restraint on the cost of tuition, it grows steadily higher each year. The fact that there aren't really any low-cost, state-funded programs adds fuel to the fire. If there's money to be made, why wouldn't the schools keep raising the prices until people stop paying them? Administrators, faculty, lenders, and in some cases private shareholders have an incentive to mislead you about the return on a chiropractic education or at least not give you the full unvarnished picture. If they did, many would lose their jobs or their investments.

Hence, most chiropractors start off with a crushing debt load. Unfortunately, I have far more serious evidence that chiropractors are treated horribly under student loan rules.

Chiropractors have almost no eligibility for the best forgiveness option, PSLF

Assume you earned your chiropractic degree and ended up with a loan amount of $250,000. You receive an offer for $60,000 a year as an associate at a practice. Your loan payments will never be enough money to touch the high balance unless you dedicate 50% of your pre-tax income to your debt. That’s not a realistic proposition.

Consider lawyers and medical doctors for a moment. In the legal profession, a student could graduate with a similar federal loan debt load and work for the government for 10 years. After this period, the government pays for the lawyer’s entire remaining federal student loan balance as a tax-free benefit. The same is true for medical doctors who work for 10 years at a nonprofit hospital. Once this service period is finished, the government covers the entire remaining student loan burden. Keep in mind this doesn't include any private loans.

Chiropractors have almost no in-field nonprofit jobs available to them. Sure, there are scattered opportunities here and there, but nothing widespread like prosecutor or public defender jobs in the legal profession or resident or attending physician jobs at nonprofit hospitals. For that reason, virtually all chiropractors graduate and take a job in the private sector.

Because of the lack of nonprofit jobs, almost no chiropractors qualify for the Public Service Loan Forgiveness (PSLF) program, which is by far the most generous benefit available to students today.

Again, there might be scattered loan forgiveness opportunities available. However, the federal PSLF program makes them look irrelevant by comparison.

Chiropractic pay is high enough to owe something each month, but not high enough to make a dent in your chiropractic student loans

Chiropractors certainly make more money than the average American household, with a median income of $70,340 across the profession as a whole. Unfortunately, chiropractic salaries are far below those of their physician peers.

Even so, chiropractic salaries are high enough to require large payments under federal income-driven repayment (IDR) plans. Paying $5,000 to $10,000 per year towards your student loans is no joke.

That said, only paying $5,000 to $10,000 on a $250,000 principal balance doesn't even cover the interest. The federal student loan rules trap chiropractors. They may have to pay significant monthly payments when they graduate, but they aren’t able to pay down their debt.

Chiropractors can still come up with a chiropractic student loan repayment strategy to save thousands

I do flat fee consults to help chiropractors save as much money as possible paying back their student loans. So, I'm very familiar with the options that do exist for chiropractors to save money on their chiropractic student debt. If you've got questions about your debt, contact me. I love hearing from readers.

Why should you believe what a random guy on the internet is saying about chiropractic student loans? Here's a quick video showing how chiropractors leave thousands of dollars on the table by not optimizing the options available to them, made by yours truly.

So, what does this video show? Most chiropractors are making a ton of student loan mistakes.

They're either paying on the wrong student loan repayment plan (e.g. IBR, Extended, Standard, Graduated, etc.) or making liberal use of forbearance or deferment. They simply might not be making optimal use of the programs that do exist.

For example, chiropractors can receive an indirect match on their 401k contributions. This match comes in the form of lower total student loan costs simply by maxing out their 401k and Health Savings Accounts.

Even so, if you want to see what I mean when I say chiropractors are truly treated horribly under student loan policy, see the deal physicians receive in the section below.

The physician loan forgiveness loophole should make chiropractors furious

Take a look at this two-minute video I made to explain the physician student loan loophole below. In this video, I show how a physician making $250,000 a year can pay less than 50% of the cost of her $250,000 medical school debt using federal student loan forgiveness programs.

What prohibits chiropractors from taking advantage of this same Public Service Loan Forgiveness program? Availability of jobs. Over 50% of all employed physicians would qualify for this benefit as most physicians are employed by nonprofit hospitals.

Doctors of chiropractic work mostly at for-profit clinics. There are very few nonprofit or government employers that hire chiropractors full-time. The ones that do exist don't need many people or might not utilize a chiropractor's skills.

For example, I searched online for chiropractic jobs that would qualify for tax-free loan forgiveness. I found one position as a health administrator for the prison system in Colorado and another job at a 501(c)(3) organization dedicated to chiropractic research.

Physician employers are tailor-made to take advantage of the government's loan forgiveness programs. That's probably due in part to the strong lobbying power of the American Medical Association. Regardless of how it happened, the difference in treatment of chiropractors compared to their peers is clearly inequitable especially given that physicians make substantially more money.

Chiropractors are treated horribly under student loan rules, and it’s the federal government’s fault

How is this you ask? Physicians work for nonprofit institutions during their training. Therefore, they qualify for super low payments during residency and fellowship that count towards the PSLF program. After 10 years of payments, the federal government forgives their debt tax-free.

Chiropractors work in the private sector as there aren't many nonprofit or government employers that hire chiropractors. That means the forgiveness chiropractors get comes after 20 to 25 years of payments under an IDR plan.

Furthermore, the United States government treats that forgiveness amount as if someone handed them a check for $500,000. This dramatically increases their taxable income for that year. So, the IRS turns around and tells you that you now owe $200,000 in taxes.

I don’t believe Congress ever worried or thought about the horrible impact on the chiropractic profession they had by passing new higher education loan rules. If I was a member of the American Chiropractic Association (ACA), I’d be up in arms.

I’d write letters to all of my congressmen and congresswomen demanding equitable treatment for chiropractors compared to their physician counterparts. The federal student loan program does not work correctly. It’s time for the chiropractic profession to rise up. It’s time to put pressure on elected officials. Chiropractors deserve fair treatment under the law.

Our business model here at Student Loan Planner® provides chiropractors and other medical professionals with solid student loan strategies. I only charge a one-time flat fee. We perform a holistic loan analysis to see what your best available repayment options are. We'd love to help you.

Comments are closed.