If you're in the teaching profession, chances are you didn’t choose the job for the money, but you had to earn at least a bachelor's degree. Dealing with student loan debt on a teacher's salary can be overwhelming.

There are loan forgiveness programs to help teachers lower, or even eliminate, student loan debt. The Teacher Loan Forgiveness Program (TLFP) is one of three student loan forgiveness programs offered by the government for federal student loans.

If you’ve thought about submitting a Teacher Loan Forgiveness application, here’s what you need to know first.

Do you qualify for Teacher Loan Forgiveness?

If you meet TLFP eligibility requirements, you can have up to $17,500 forgiven from your student loan principal. However, the award amount depends on which academic subjects you teach.

Science teachers and others in the STEM field (e.g. mathematics, technology or engineering) may be eligible. Special education teachers can also receive the maximum forgiveness amount.

Educators teaching subject areas outside of STEM and special education can receive a maximum $5,000 in teacher cancellation benefits. Below are the qualifications needed for loan forgiveness under this program.

You must be a classroom teacher

You must be a teacher with direct classroom teaching responsibilities in order to be eligible for the program. School administrators, counselors, librarians and other educational service staff don’t qualify. They should look into one of the other federal forgiveness programs instead.

You must be a highly qualified teacher

There are two requirements to be a highly qualified teacher. First, they must have obtained a bachelor’s degree. Second, they must have received full state certification as a teacher. Additionally, this certification or license must never have been revoked, waived or suspended.

If you’re new to the teaching field, work for a nonprofit private school, or teach at a public charter school, you need to prove you’re highly qualified. You're required to have completed and passed rigorous state testing in your specific subject knowledge area or demonstrate a high level of competency for all subjects if you teach K-8.

You must be employed at a low-income school

You need to have worked at a school or educational service agency that serves low-income students. All Title 1 schools qualify as low-income schools.

Even if you only worked some of your five years in a low-income school, you can still qualify. If you’re not sure your school qualifies, search the Teacher Cancellation Low Income directory. The TCLI directory serves as an annual directory of designated low-income schools.

You must work full-time for five years

Lastly, you must be a full-time teacher for five consecutive, complete academic years. Full-time is determined by your Full-Time Equivalent (FTE) status. Your five consecutive years need to be without any breaks or changes in order to be consider qualifying teaching service.

There are exceptions to this rule. For example, say you worked a half year and took approved maternity leave. Then, you returned to work. You'd still be considered as having completed your contract and can be eligible. Because the time you’re gone is approved and under contract, it’s a part of the five years required for loan forgiveness.

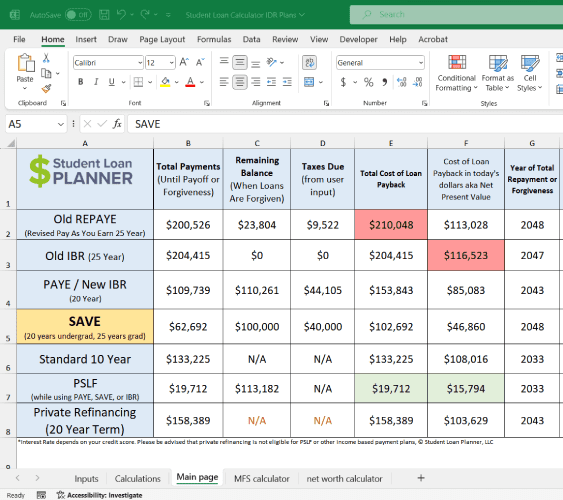

Get Started With Our New IDR Calculator

Are your loans eligible for forgiveness?

The TLFP can forgive Direct Subsidized and Unsubsidized Loans (also known as Federal Stafford Loans).

All loans must have been taken out after Oct. 1, 1998.

If you consolidated your federal loans or PLUS Loans with a Direct Consolidation Loan, your loans are still eligible.

Your accounts should also be in good standing. If you’re in default or have an outstanding balance on a Direct Loan or Federal Family Education Loan (FFEL), you aren’t eligible.

Private student loans aren’t eligible for forgiveness. If you have private student loans, you may want to look into student loan refinancing.

Steps to complete the Teacher Loan Forgiveness application

Do you meet the qualifications above? After working for five academic years, complete the Teacher Loan Forgiveness application. Prepare your student loan documents, and know how much in forgiveness awards you’re eligible for. Verify your school’s status and eligibility so you can check off the right boxes.

1. Fill out the official application for Teacher Loan Forgiveness

Print the Teacher Loan Forgiveness application, and fill out sections one through four on your own.

- Section one: This section asks for personal information, like your Social Security number.

- Section two: Provide your school’s information. This includes where you taught and your teaching assignment during the five years.

- Section three: Includes details from those who have applied for Teacher Loan Forgiveness before. If this is your first time submitting a Teacher Loan Forgiveness form, simply mark the corresponding box. If you previously applied for Teacher Loan Forgiveness, fill in the required information for the lender and the loan you requested forgiveness for.

- Section four: Provide your authorization and signature that the information on the form is correct.

If you have trouble completing section two, reach out to your Human Resource Department for your school’s details. As you complete the form, you can refer to sections seven and eight for directions and definitions.

2. Reach out to the Chief Administrative Officer of the school you work for

The Chief Administrative Officer (CAO) at your school completes section five of the form. Typically this is a superior who has access to your education file and can verify your qualifying employment.

The CAO could be your principal, assistant principal or superintendent, depending on your employer. In some rare cases, a human resources official can sign the form for verification.

3. Send the form to your loan servicer

Visit your student loan servicer’s website or give them a call for the correct address to send the Teacher Loan Forgiveness application. Make a copy of the application for your records before sending it out.

Processing time depends on your student loan servicer. Ensure you have your online account updated with current contact information, and check in with them if you have questions. Continue making monthly payments and keep your account in good standing while you wait.

Teacher Loan Forgiveness form: Special circumstances

Borrowers may have special circumstances, like working at multiple schools or having your loans in more than one place. If this is the case, you have a few more steps to complete before submitting the application:

- If you taught at different schools: If you taught at different schools during the five years, the CAO from each school will have to complete section five. Submit the additional pages with your full application.

- If you have multiple program loans with different loan servicers: You need to have a separate application for each loan if the amount being forgiven is greater than the principal of a loan. For example, say you qualify for $17,500 in forgiveness, and you have a $15,000 student loan with one servicer and a $5,000 loan with another. You would need an application for both of the loan servicers.

If you don’t know how many loans or servicers you have, check your Federal Student Aid account. It should have a record of all your student loans and loan servicers.

Common Teacher Loan Forgiveness application mistakes

The Teacher Loan Forgiveness application is wordy. It’s easy to make mistakes when you’re filling out the form. Avoid these common errors on the form itself to avoid delays:

- Submitting the application before the five-year mark results in automatic denial.

- The CAO may forget to include their official title. Triple-check their entry box in section five before sending it in to ensure a full title is present.

- Your teaching dates must be current and specific to what is in your file. Include the month, day and year for the beginning and ending dates. Don’t put in “present” as this will result in rejection.

- Middle school teachers or those who work in blended schools like K-8 often select “Elementary School.” This is because they typically consider secondary education to be only high school grade level. However, the type of school you select on the application must be what's documented by the state. You can get this information from your Human Resources Department.

If you make a mistake on the application and it’s denied, you can always submit a new one. But you can avoid that and save yourself some time by verifying the information on the application before submission.

Consider other forms of student loan repayment

While the TLFP is helpful, it may not be the right loan cancellation program for your undergraduate or graduate degree student loans. The Public Service Loan Forgiveness Program (PSLF) offers forgiveness for federal student loans after ten years of qualifying loan payments under an eligible repayment plan.

You can stack the TLFP and PSLF, but you can’t stack teaching years. If you receive Teacher Loan Forgiveness after five years of teaching, the clock resets for the ten years of qualifying payments required for PSLF.

Every situation is unique. If you’re a teacher with a large amount of debt, you may want to consider a professional consultation. A low salary doesn’t mean you can never pay off your debt or save for the future. Reach out to one of our consultants, and start taking control of your debt payoff plan.

Not sure what to do with your student loans?

Take our 11 question quiz to get a personalized recommendation for 2024 on whether you should pursue PSLF, Biden’s New IDR plan, or refinancing (including the one lender we think could give you the best rate).

Comments are closed.